CPF, in short for Central Provident Funds, is a "social security system that enables working Singapore Citizens and Permanent Residents to set aside funds for retirement. It also addresses healthcare, homeownership, family protection and asset enhancement.".

Source: https://www.cpf.gov.sg/Members/AboutUs/about-us-info/cpf-overview

1. CPF Education Scheme

This scheme allows you to use your Ordinary Account (OA) savings to pay for your own, children’s or spouse’s subsidised tuition fees. Applications can also be made to use CPF savings to pay for your sibling’s or relative’s subsidised tuition fees but will be assessed on a case-by-case basis.

However, one point to note is that this is effectively a LOAN from whoever's CPF you are using to pay for your education. Hence, it is necessary to pay back this loan with interest. The effective interest rate payable is then pegged to the OA interest rate, which is adjusted quarterly.

The student has to start repaying the loan one year after graduation or termination of studies, whichever is earlier. Repayment must be made in cash either in one lump sum or via monthly instalment over a maximum of 12 years. The minimum monthly instalment is $100 and the rate will be computed for the student based on the loan amount and repayment period.

2. CPF Investment Scheme

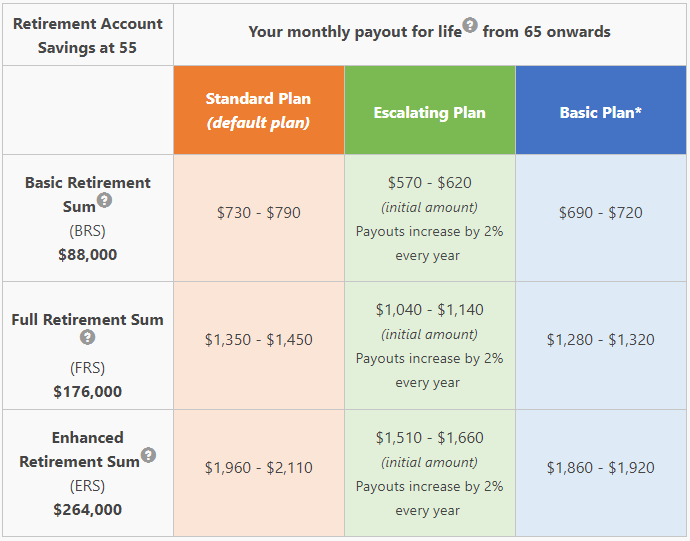

As we graduate and take on our first job, it is imperative to consider investing for retirement. If you are thinking of that, then this is the scheme that you do not want to miss out. This scheme allows you to invest your Ordinary Account (OA) and Special Account (SA) savings in a wide range of investments.

- are at least 18 years old;

- are not an undischarged bankrupt;

- have more than $20,000 in your OA; and/or

- have more than $40,000 in your SA.

You can find the range of products which you can invest in here. One of the products is Exchange Traded Funds (ETFs) which our blog had been advocating!

Find out more here:

- Singapore Growing ETF Choices

- ETFs VS Hedge Funds

- How much can I invest in ETFs using my CPF?

- Key Takeaways from The Edge ETFs Forum 2015

3. CPF Nomination Scheme

We might be thinking we are so young, filled with hope and energy. Death might be the least of concern. This is especially so after the recent hoo-hah, where CPF stated that CPF funds are not covered under a will.

For more info: https://www.straitstimes.com/forum/letters-in-print/cpf-monies-not-covered-by-a-will

The nomination procedure is very simple.

All you have to do is fill in a form found on the CPF Nomination Website.

Download the form, fill it up and submit it to CPF Board.

Here are some other information that are useful to you!

More information can be found here: https://www.cpf.gov.sg/Members/schemes/schemes/other-matters/cpf-nomination-scheme

For more info: https://www.straitstimes.com/forum/letters-in-print/cpf-monies-not-covered-by-a-will

The nomination procedure is very simple.

All you have to do is fill in a form found on the CPF Nomination Website.

Download the form, fill it up and submit it to CPF Board.

Here are some other information that are useful to you!

What does a CPF Nomination cover?

| Covered under CPF Nomination | Not covered under CPF Nomination |

|

|

More information can be found here: https://www.cpf.gov.sg/Members/schemes/schemes/other-matters/cpf-nomination-scheme

Conclusion

CPF is definitely not an organisation for the elderly. In fact, youngsters should harness such national scheme, especially since it affects us for the long term!

Remember to offer your opinions. If you don't put your two cents in, how can you expect to get change?

Have feedback? Tell us now!

Subscribe to us or

Follow us: Investment Stab on Facebook

Unhappy with your job? There's something you can do about it.

A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort

B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below.

They can link you up with the career coach and you might be able to find new opportunities on their jobs portal.

http://ow.ly/GY8150wlfrF

Remember to offer your opinions. If you don't put your two cents in, how can you expect to get change?

Have feedback? Tell us now!

Subscribe to us or

Follow us: Investment Stab on Facebook

Unhappy with your job? There's something you can do about it.

A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort

B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below.

They can link you up with the career coach and you might be able to find new opportunities on their jobs portal.

http://ow.ly/GY8150wlfrF