Singapore-based financial blog that aims to educate people on personal finance, investments, retirement and their Central Provident Fund (CPF) matters.

What is Share Buyback?

It is the company buying back shares of itself to reduce the number of shares outstanding, and in return increase the value each share is worth.

For a more in-depth explanation about it, refer to the Investopedia page HERE.

Why Companies (particularly US companies) Love Share Buyback?

The main reason: Tax

In the US and other countries, shareholders have to pay a dividend tax for the dividends they receive.

In the US, the nominal tax rate is 30%.

This causes shareholders to experience double taxation - once on the company's profits, then again on the dividends paid out of the profits.

To avoid double taxation, companies use share buybacks as a way of "giving" returns back to shareholders.

The math of Share Buybacks You can skip this if you know how buyback works

A company made $1 million in profits, has 1 million shares outstanding, and a PE of 10.

The current share price of the company is $10, and the Earnings Per Share (EPS) is $1.

If the company bought back 10% of its shares (100,000 shares), the EPS will increase from $1 to $1.11 ($1m profits / 900k shares).

Assuming the PE of 10 does not change, the new share price will become $11.11 (an 11% increase just by reducing the share count by 10%).

Recommended Read: How I Saved $1000 of my $2500 Salary The Math Portion of Why Buyback Is Better Than Dividend

A company made $1 million in profits, has 1 million shares outstanding, and a PE of 10.

The current share price of the company is $10.

Assuming the company grew earnings by 4% this year, the new share price will become $10.40.

Assuming that the company pays a 2% dividend, which means it will pay out $200,000 in dividends.

As a shareholder, you will earn 6% this year.

Now, instead of spending $200,000 in dividends, it used the $200,000 to reduce the shares outstanding via a share buyback.

At $10 per share, $200,000 will buy back 20,000 shares or 2% of the shares outstanding.

With a 4% growth rate, profit becomes $1.04 million, divide by 980,000 shares, the EPS becomes $1.06.

The new share price will become $10.60, you as the shareholder will still earn that 6% return.

Problem with Share Buybacks in Singapore 1. Dependence on the Company Performance

When you get a dividend, it is cash into your pocket you can use to invest in other companies or buy things you like.

When you get buyback, you get no cash, but your ownership in the company increases.

If the company grows and earns more, your increased ownership in the company will be worth more.

But if the company shrinks, your ownership in the company will be worth less - worse still, you have no dividends to help you cushion the blow or to use as funds to buy more of the company's shares at a lower price.

2. No Tax Efficiency

In the US (and other countries), dividends are taxed, but share buybacks are not.

Hence from the shareholders' perspective, it might be better to spend cash doing share buybacks than paying out as dividends to avoid taxation.

But in Singapore, dividends are tax-free.

So the idea that "buybacks are better than dividends because of tax advantages" no longer works in Singapore's context.

3. Management Problems

I often tell my friends the statement below when explaining why I prefer Singapore companies do dividend over buybacks.

"I much rather they give me the cash and let me decide what to do with the money than let management hoard the cash. Rather I make a mistake with my money and lose it than for management to make a mistake with my money and lose it."

Of course, there are good companies that really make great use of shareholders' money to reap even higher returns, like what Warren Buffett did for Berkshire Hathaway.

But then again, how many Warren Buffett and Berkshire Hathaway do you really see in the world?

The probability of investing into the next Warren Buffett or Berkshire Hathaway is fairly low actually.

4. Company Problems

IBM spent US$83 billion on share buybacks over the past decade, but the stock price and market capitalisation went nowhere.

As an investor of IBM, it might be better had they just gave all that US$83 billion out as dividends.

Even though shareholders have to pay taxes, but at least they will still have US$58 billion and a shrinking company, instead of now where they have no cash but huge ownership in a shrinking company.

Conclusion

Share buybacks can be great for shareholders if they are done correctly.

Except it is really difficult for it to be done correctly.

Warren Buffett (world's greatest investor) set a limit on his buyback activity - he would only buy back shares if the share price fell to below 1.2x his company's book value.

At 1.2x, he considers his company to be undervalued enough to justify buying back shares and benefiting those shareholders who held on to their shares.

Unfortunately, most management teams do not have such discipline - particularly so since almost no management will ever say their share price is undervalued, even if it is significantly overvalued.

Hence, it might be better, if we as shareholders demand higher dividend payouts and fewer share buybacks!

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

What is Mortgage Insurance?

It is an insurance plan the homeowner buys when they buy a home with a loan.

In the event that the owner passes away, or suffers from a terminal illness or permanent disability, resulting in his/her inability to pay the mortgage, the insurance will pay the remaining balance of the mortgage.

What is the CPF Equivalent?

It is called the CPF Home Protection Scheme.

You must buy this insurance if you are using your CPF to pay for your HDB mortgage.

It is automatically deducted from your CPF OA every year when it is up for renewal.

For more information about this scheme, click HERE.

Why does it Suck?

The premium you pay is fixed for the whole period, eg if the premium $300 per year when your outstanding mortgage is $400,000; the premium will still be $300 after 20 years even though the outstanding mortgage balance would have dropped to $50,000.

If the owner passes away during the first year of the insurance, the insurance company will cover the full $400,000 of the mortgage.

However, if the owner passes away 20 years after buying the HDB, the insurance will only pay the $50,000 outstanding to cover the mortgage, even though the owner has paid $6,000 ($300 x 20 years) worth of premiums.

But, if instead of buying an HPS, you instead bought a life insurance policy.

The cheapest 30-year term-life insurance plan we found on CLEARLYSURELY cost $368 per year - a little more expensive than the HPS.

But, the thing here is, if the homeowner has a life insurance instead of a mortgage insurance, whether the homeowner passes away on the first year or the last year while the mortgage is still outstanding, the dependents would get the full $400,000 instead of just an amount that is sufficient to cover the mortgage.

So the dependents can use the $400,000 to pay off the outstanding mortgage, and any amount of leftover can be used for funeral cost, living expenses, etc.

What's the Good News then?

You can apply to be exempted from the CPF HPS.

If you have one or more of the following policies:

Whole life

Term life

Endowments

Life Riders (must be attached to a basic policy)

Mortgage Reducing Term Assurance (MRTA) / Decreasing Term Rider

In addition, these policies must cover the outstanding housing loan up to the full term of the loan or 65 years old, whichever is earlier.

The exemption can also be revoked if any of the insurance policies used for the exemption is discontinued or altered.

So, if you are considering buying an HDB and paying for it with your CPF, you might want to consider replacing the CPF HPS policy with a term life insurance policy.

Recommended Read: How I Saved $1000 of my $2500 Salary

Remember to offer your opinions. If you don't put your two cents in, how can you expect to get change?

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

Today we will be answering this question: How much is my Dependents' Protection Scheme (DPS) premiums?

DPS is a term-life insurance scheme that provides your family with a lump sum of $46,000 when you:

1) suffer from a terminal illness or total permanent disability

2) passed away

Its is term insurance and is meant to insure you until you reach the age of 60. In simple words, it is a term life insurance that insures you up to $46,000 and is paid by your CPF money. The insurance premiums are paid annually and the rates are as per below.

If you would like to know how to save on your monthly insurance cost, link HERE

Age (as of last birthday)

Yearly Premiums

34 years & below

$36

35 - 39

$48

40 - 44

$84

45 - 49

$144

50 - 54

$228

55 - 59

$260

Assuming you started contributing to your CPF at the age of 16 (our first part-time job) and bought this insurance since then and continued it till you reach 60 years old, you would have paid out $4,504 in premiums for a $46,000 protection - sounds pretty worthwhile?

By comparison, a private term-life insurance plan would cost more for the same amount of coverage.

So for 45 years of coverage, the CPF DPS worked out to about $100 per year in premium paid.

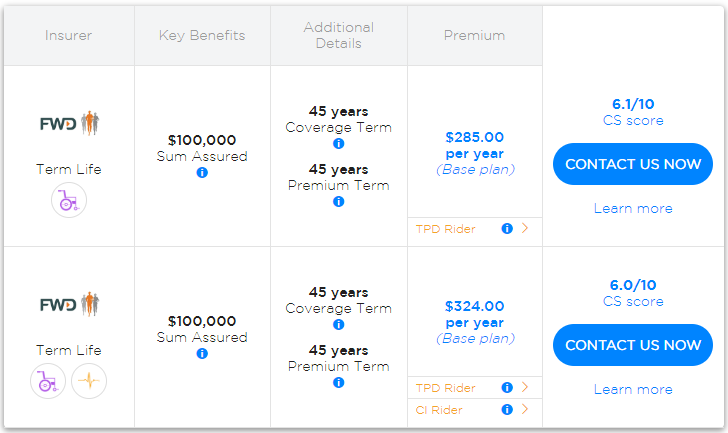

We did a search on ClearlySurely for the cheapest $100,000 term-life with 45 years of coverage, and it worked out to $285 per year in premiums (or $131 per year for $46,000 of coverage if we calculate it ourselves).

So private insurance is 30% more expensive than the CPF one.

Of course, just relying on the CPF one alone is not enough - you might need more protection for your family members and you probably need to supplement it with private insurance.

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

Here's a story (or break down) of how I spend my money every month.

Salary: $2,500 per month

Expense: $1,500 per month

$300 to my parents

$700 for food (breakfast, lunch, and dinner), entertainment, transport, phone bills

$300 towards student loan repayment

$200 for surprise expenses and insurance

I managed to save $1000 saved every month.

Sure it helps that I'm single, am a guy (statistically speaking it is cheaper to be a guy), no family to feed (no kids no wife), no housing loan, no car loan, etc.

The only expensive thing is eating out every day, but that's not too bad in Singapore, compared to other countries like Australia, etc.

I also try to stretch my student loan - not pay it down too fast, and I stated the reasons why in another article that you can read HERE.

My "amount of money saved per month" is not the best - I know a lot of people who get by every month spending even less than me, but it’s about saving a big enough portion of your pay while being happy, and everyone spends different amount to stay happy 😉.

After all, I’m a millennial who needs his Starbucks and stuff every once in a while.

There are temptations nonetheless and I'm constantly trying to fight them so that I can save more money.

Temptation Number 1: Buying New Clothes

I have about 8 sets of office attire but wears only 7 sets of them (I try to avoid my white shirt because they can be hard to wash and maintain).

Some times I feel like my wardrobe selection is so limited that it would not hurt to get a couple extra sets of work clothes.

But honestly, I always wear a jacket at work because it is cold.

No one can see what I'm wearing underneath.

So it does not make sense to buy something that no one is going to see most of the time.

Besides, for a guy, it's common to wear a white shirt and black pants daily - it's like a uniform.

No need for variety - that's 1 less headache every morning thinking about what to wear.

For women, I guess it's tougher. I heard from female friends that their colleagues would talk about what they wear to work and stuff, so it's probably tougher to always wear for the set of clothes for them?

A friend of mine told me that since she started working, her wardrobe expanded from 8 sets of work clothes to almost 30 sets - that's a lot of money spent on clothing 😱.

Temptation Number 2: Coffee

Coffee

Starbucks, Coffee Bean, or just the Kopi at the coffee shop below my office.

These all cost money.

What's worse is that my office provides free coffee and tea 🤦♂️

Somehow, Nescafe, 3-1 instant coffee, or the coffee machine that brews coffee straight from the beans just does not taste as good as the $1.60 kopi-peng from the coffee shop below my office.

Suddenly, after making some money, the need to buy decent coffee to start the day right seems important.

To make matters worse, I am actually trying to kick the habit (addiction) of drinking coffee.

Nonetheless, some things just cannot be avoided, and I guess the unnecessary coffee habit is going to continue 😢.

But, if you can avoid this, try to avoid this, you can save $8 per week or $32 per month just by drinking coffee provided by your office!

That's like a decent meal at Din Tai Fung! 🤤.

Temptation Number 3: New Devices

"I need a new phone", "I need a new laptop", "I need a new iPad", "I need this, need that".

How many of us fall into this trap?

Suddenly, because we can afford it, we start to find justifications to why we need new things in our life.

"I need a new iPad so that I can write more blog posts on my bed!".

Yup, that's the excuse I'm selling to myself to convince me to get the new iPad 😎.

That's the idealistic voice telling me to reward myself.

Then there's the practical side of me going "your laptop can fold into a tablet, if you really want to do work on your bed, you can use that laptop. But chances are you will not do any work on your bed because you are lazy".

On the bright side, team Practical seems to be triumphing over team Idealistic so I managed to control and not splurge on a new iPad.

Nonetheless, I still browse through Apple's website and store every once in a while, to admire the beauty of the product that I did not buy 🤣.

Conclusion

Instead of having strict budgeting rules and skipping the Starbucks, I follow the more flexible money management rule of 50-30-20.

And it sure seems that I'm well within the limits.

60% of my salary is spent on 'Wants' and 'Needs' instead of 80%.

40% of my salary is saved and invested instead of just 20%.

So I guess I am doing pretty okay.

What about you?

What are some of the temptations you face when you started working?

Let us know in the comments section😁

And if you like our memes or tips, follow us on Facebookor Instagramto view more of it.

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

Today's post is an answer to the question: Why do I have to return into my CPF account the accrued interest I accumulated?

This question is posted by one of our readers.

We would like to thank him/her for reading and interacting with us by posting a question for us to answer.

If you have any more questions regarding this topic, feel free to comment, ask us, or email us.

We would love to hear from you on how you think about this topic or other things that you would like more details/clarity on.

1) What is Accrued Interest?

The CPF Housing Loan Accrued Interest is the interest that you would have accumulated if you had not used the money in your CPF Ordinary Account (OA) to pay for your monthly mortgage.

So because you took it out, it could not earn the accrued interest, so that 'interest charge' is accumulated.

However, the accrued interestDOES NOT belong to the CPF. It belongs to you.

The accrued interest goes back into your CPF OA account.

2) Why do I have to return the Accrued Interest?

Assuming you did not use your CPF to buy your house, your CPF OA balance would have earned an interest of 2.5% every year from CPF.

That money will be kept inside your CPF and would continue growing every year.

When you sell your house, you return into your CPF OA the amount that you had taken out to pay for your house (principal), plus the interest you would have earned if the principal was not withdrawn to pay for your house.

The "returning of CPF principal + accrued interest' is so that your CPF OA account can fully reflect the amount that should have been inside if you did not use it to buy a house.

I would say there are 2 big reasons for this:

a) Keeping the money inside CPF ensures that you can hit your minimum sum faster.

b) Discipline, because people tend to spend the extra cash once they profit from selling a house, thus if a portion of it went into a place that they cannot withdraw and spend, the money is thus saved. Recommended Read: Moving CPF RSS to 90 is a Good Social Experiment

3) Am I Paying Double Interest via CPF Home Loan?

In a way, yes. You are paying interest to the CPF at a rate of 2.5% + 0.1% (base OA interest rate + 0.1%). Also, you are required to return back into your OA to the "would-be amount" if you did not use your CPF to pay for your mortgage (OA rate of currently 2.5%). BUT, you can also consider it as a mortgage loan + forced savings.

You pay your monthly mortgage, and upon selling your house, it automatically helps you transfer some of your money away into a savings plan (forced savings), which you can use for a range of different purposes depending on your age and schemes available.

4) What if I Don't Want to Pay the Accrued Interest?

Well, there are 2 ways:

Pay for your home with cash and not with your CPF money.

Don't ever sell your house. You only have to return the money into your CPF if you sell the house. If you never sell, you never need to return.

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

If you have not heard, CPF members who are on the older Retirement Sum Scheme (RSS) will now have payouts lasting up to age 90, down from the previous age of 95. Here's a link to the article.

Illustration:

If you are retiring at age 65, is not on the CPF LIFE Scheme (aka you are on the RSS), and has $50,000 in your CPF Retirement Account (RA).

Previously, when the payout would last until you are 95 years old, your monthly payout would be about $235 ~ $295.

Now, after the changes, your monthly payout would increase to about $260 ~ $315, almost 10% increase!

Now, the numbers here are for illustration only because we don't have access to the actual calculation method, but we expect the numbers to be fairly close to our estimates.

This is great in 2 ways for those on the RSS scheme.

1) Those on the RSS scheme tend to be of the older generation (born before 1958) and the average life expectancy for this generation is estimated to be about age 83 or even longer. Correction: So 90 years old sounds like a good enough number with some margin of safety.

2) Those born after 1958 but *do not have significant savings in their CPF RA* will also be under the RSS, and shortening the payout period would greatly increase their monthly payout - which is great.

*do not have significant savings in their CPF RA* are those who fit the condition below.

Commentary:

Now, this part is just how I feel, and not necessary is the Government's stance.

But I think this is a pretty good social experiment.

I feel that this is a test on how citizens would react when they realise that they have run out of retirement money in their golden years because they have used up their CPF money.

There are so many people complaining that CPF is their money and that the people should be able to choose if they want to withdraw the whole sum out at age 65 (or 55) or leave it inside CPF.

The CPF stance has pretty much been "We care for you and your retirement, we are afraid you might mismanage the money and end up going broke during your retirement. So we take care of your money and give it to you in monthly payouts so that you can live comfortably."

Unfortunately, not a lot of people are convinced by that narrative that CPF tries to sell us - even though it is true (many people cannot handle a sudden windfall of money and often end up broke within a few years after getting that large sum of money).

So to me, this is like an experiment to test if people would complain when they run out of money in their retirement.

It is tested out on a small group of Singaporeans (those born before 1958 or those with little CPF savings), so the negative impact of it is minimised.

And we have heard people say "If we run out of money during our retirement, it is our problem! You (Government or CPF) don't have to worry our us!"

Now, we might have a way to put that statement to the test 😉

If we hear complains from people saying that are miserable, they are suffering, that the Government and CPF is not helping them when they reached 91 years old and have run out of CPF/retirement money, then we know for sure that the general folks cannot handle their money, and maybe, it is best to leave it in the hands of professionals.

What do you think?

Do you think this is a good social experiment also?

Or do you think this is a good change and it shows that the Government is actually listening to our demands?

Let us know in the comments! 😊

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

There are many Big Tech companies, and they are either added or dropped from the list very fast.

From the initial FANG (Facebook, Amazon, Netflix, Google), to the FAANG (the 4 + Apple), or GAFAM (Google, Amazon, Facebook, Apple, Microsoft).

But for our case, we are just going to talk about the Big Four: Amazon, Apple, Facebook, and Google.

I was watching a video from Scott Galloway - a business professor from New York University, talking about the problem with Big Tech and he gave a point of view which I thought was pretty interest.

If you are interested in the talk, here's the video (it's about 20 minutes long).

But the interesting point he made that stood out to me was the sheer size of human capital these Big Techs hires and what they do with their human capital.

The Manhattan Project, the creation of the nuclear bomb, which ended WWII and brought world peace ✌ had almost 130,000 people working on the project.

By a similar number, Facebook and Google hire a total of 134,000 people, and what they did was to try and predict and show you another ad so that you would click.

Don't hear it from me, the Prof from the video said so, so did Li Hong Yi (PM Lee's son)

Of course, this is an interesting perspective but definitely not all true.

Without Google, you won't be reading this article (powered by Blogger, which is owned by Google), you won't be able to watch the video I added above, either would you be able to navigate in a foreign country (or even your own country without Google Maps).

And we definitely need Facebook to know what new branded bag our friends bought, who broke up with their partner and started ranting on social media etc.

Amazon and Apple hire almost double the number of people in the Apollo Project, their main goal is to sell you another iPhone (you can buy it on Apple stores or Amazon website).

Sure, Apple is focused on creating the best product and Amazon is focused on creating the best customer experience.

No one thought they needed to use their face to unlock their phones until Apple did it and suddenly everyone's like 'OMG! This should have always been the way to unlock a phone.'

And if we don't have Amazon, there won't be Amazon Web Services (AWS), the cloud provider that powers between the bulk of the internet. Netflix and Slack are just 2 examples of companies running on AWS, in addition to many other governments and companies.

Conclusion

There are always 2 sides to everything. Technology is a 2-edged sword: you can benefit from it, or get hurt from it.

We connect with our friends and families via social media, but many are also cyber-bullied via these platforms.

We get information and knowledge via search, but many newspapers are losing revenue because of falling ad revenues.

We get products delivered to our doorstep fast, but many small businesses (and big retailers) are going bankrupt.

We get the best quality devices and services, but many other companies that are offering similar services get crushed via competition from the platform owners.

Do I have a solution? Nope, I don't.

I still want to watch YouTube videos for free (so I'll watch the ads, even though now you can get YouTube Premium to not watch ads in your videos).

But I'll use 'Sign In with Apple', to limit the data that companies are collecting on me when I use their services.

It is about making choices, and it always helps if we have clearer and better information about what are we getting, and what are the trade-offs.

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

I just ended a 24 weeks internship at the Government of Singapore Investment Corporation (GIC).

In case you do not know what's GIC, it is one of the sovereign wealth funds that invest Singapore's reserves on behalf of the Singapore Government - the other is Temasek Holdings.

About GIC

GIC has 2 goals

1. To preserve the long-term international purchasing power of Singapore's reserves placed under its care.

2. After achieving 1, it proceeds to enhance the long-term international purchasing power of Singapore's reserves placed under its care.

Simply put, its job is to first and foremost provide returns that match the global inflation rate (preserve purchasing power). After achieving that, it then tries to invest and earn a return above that global inflation rate.

Actually, over 20 years, GIC has achieved an annualised 3.4% return ABOVE the global inflation rate (AKA if the global inflation rate is 3%, GIC's return was 6.4%).

Alright, now that you have read some background information about GIC, it is time to read what I have learnt.

But before you continue reading, I would like to warn you that this is going to be very long.

So if you are in the middle of doing something important, bookmark this article to read later.

Brief Information on my Role

I interned in the Technology department - no, not the technology investment department (though I wish I did).

I interned in the Technology department - as in the department that manages and develops all the tech/software that keeps GIC running.

My role is to develop software and applications for GIC's employees to use in their daily work.

So if you are hoping for some investment tips, I'm sorry, there aren't any.

1. Ask, Don't Reinvent the Wheel

There were many instances during the internship where I spent time exploring and experimenting on solutions and ideas that others before us had already completed. Asking people might be faster than Googling for unclear answers and had I asked more often, I might be able to save more time and worked on more tasks. But I think the first thing we as people have to do is to overcome the stigma or fear of being seen as always looking for shortcuts and the idea that if someone is constantly asking for help, it means they are lazy and not willing to do their own research. We have to understand that if someone comes to us for help and if we help them, they can get work done faster, and they will gain experience, and that is a great thing. But we have this stigma that if we give them everything, then they would not learn; but everyone learns differently, and some people learn by breaking ready-made things apart, reverse-engineer, and learn from it. 2. Enterprise are Technologically Backward

While startups and new companies use applications like Slack for their internal communication, many old enterprises are still using Email (Microsoft Outlook) and Skype. In modern times, collaboration is important, we could simultaneously work on the same document via Google Docs, but when it comes to our workplaces, we end up creating a Microsoft Word doc, send that Word doc to our supervisors for vetting, our supervisors come back with their comments, we then make the changes before sending the document back to them. We make so many copies of the same document and sending them back and forth when all these could be reduced if we simply just used a collaboration tool like Google Docs. On a side note, Office 365 now offers online Office Suite, and you can collaborate simultaneously with your colleagues on the same document now - so do check with your company if you are subscribed to that service. If your company is using Microsoft Office, start using their online version of the software so that you can collaborate instead of creating multiple copies of the same document. But given that people are often reluctant to change, I think unless the on-device Office applications are removed, people will probably not move over to the cloud/online version of the product and will continue to use Email as the primary tool for sending and transferring documents. 3. Culture is Important

I had learnt earlier from my other internships that culture is important, that it is possible for some people to not be able to fit into a certain company’s culture. The problem with culture is we will never know how it is like until we get into the company, and we will never know what culture fits us until we tried a few companies to know what we look out for. Personally, from my previous experiences, I learnt that I am not interested in companies that are focused on time spent in the office. An example would be like a company that requires employees to be on time or be at their desk most of the time during working hours. I think everyone works differently and works best in a different environment, some may like being bound to their desk, while others like myself, prefer to work in a different environment – some times at the desk, some times in the pantry facing the view outside the building, et cetera. To me, it is more important that work is completed on time (regardless of where I am doing my work) than spending exactly eight or nine hours per day sitting at the same desk, especially so in modern times where the workforce is mobile. Don't hear it from me, hear it from the great Mr Wonderful, Kevin O'Leary from Shark Tank.

If you are wondering about GIC's work culture, it is actually kind of in line with mine: as long as work is done, all is good. GIC practices flexi-hours, allows employees to work from home if needs be (usually for parents who needs to take care of their sick children), and practices open office and hot-desking, which is great since I can get a change of environment and let the brain “stretch” a little as well, which helps when I am stuck on a certain problem. 4. Find Interesting Tasks To Do

“If you do what you love, you’ll never work a day in your life”, these were the words from Marc Anthony. While I do agree with this quote, I do not think that we can be that lucky to have a job that always lets us do what we want; even if you are the boss of a company, there will be business matters that you hate to do but have to do it anyway. But, I do think that it is possible (and important) to be spending more of your work time on tasks that interest you. If the task interests you and has a purpose, then it becomes more than just a task, but like a stage in a game that you want to conquer – which is why gamification of work is getting more prominent in workplaces. I had my fair share of tasks that are interesting and meaningful, and some that were not so much of both, so I think it is a pretty good mix. Below is a table of how I view tasks; doing tasks in the green box is the best (tasks that interest you) and it is important to try and avoid the tasks in the red box unless there is no choice.

Nonetheless, I still completed the tasks assigned and you should too! As Amazon.com CEO Jeff Bezos says it, we can ‘disagree and commit’. We can disagree on what is the best solution for a given task but once it the solution is decided on, we will give our best to get the solution done.

5. Make Faster Decisions

Facebook’s founder Mark Zuckerberg’s motto used to be ‘move fast and break things’, which was how he navigated and dominated the social media space. Amazon.com founder Jeff Bezos says that decisions should be made with just 70% of the information because waiting till 90% would be too late, and most decisions made are reversible if proven to be wrong down the line. Both of them placed emphasis on one thing: speed. Technology changes very fast, decisions that were made yesterday might become obsolete by today because of a new technology breakthrough. Instead of waiting for more information or confirmation, sometimes the best course of action is to Just Do It.

During my internship, I would have debates with my supervisor over which solution to implement. But that caused a simple five-minute discussion to drag into a 30-minute long debate; which I thought was just time wasted. Eventually, I would just voice my opinion or solution, and if it was not taken, I would let it be and focus on working on the chosen solution – essentially putting that 25 minutes of discussion time into product development. If the chosen solution fails, then we would fall back on my solution. Most of the solutions are for the product’s small components and the impact on the product would not be huge; and if we were wrong on the chosen solution, they were easily reversible.

Like Jeff Bezos said, there are 2 types of decisions, and most decisions belong to Type 2. But large companies have the tendency to use Type 1 framework on Type 2 matters, which slows down progress and leads to frustration. So make sure you use the correct method for the corresponding decision. 6. Have Clearer Communication

Tesla’s CEO Elon Musk once lamented that the excessive use of made-up acronyms within an organisation would inhibit effective communication and that it should be cut down to the minimum. Amazon’s founder Jeff Bezos banned PowerPoint in Amazon.com, choosing to instead have employees to write a six-page, narratively structured memo. The emphasis here is on clarity – getting the message across with minimal understanding lost. I saw my team spent a lot of time working on their slide deck to present their solutions to the senior managers. I thought that time would be much better spent if instead of a slide deck (which requires time spent on the design, animation, etc.), a six-page narrative might actually work better in conveying the information that they wished to convey. It is clearer than icons and provides a source of reference that is there instead of relying on their memory on what was discussed or on the minutes which might not fully record the meaning behind what was said. Acronyms were another hindrance, with terms like EDMS, etc. that made no sense to someone who has not been with the organisation for longer than one month. Even though we did ask what they meant, my brain could not remember every single one of them and eventually I gave up since most of the acronyms I heard I ended up not having the need to deal with them – it is like they are rarely used so why even have an acronym for them in the first place?

7. Have Fewer Meetings

Tesla’s CEO Elon Musk set three rules for more effective meetings in his companies.

No large meetings (maximum 6 people)

If you are not adding value to the meeting, leave

No frequent meetings.

While it is true that everyone finds meeting a waste of time, no one actually leaves a meeting even if they are not adding value – unless they have something else on. You will have a room of associates, managers, supervisors, or more, all in a meeting listening to the discussion, with most of them bring quiet most of the time and some gave inputs once in a while when asked. But we would not leave these meeting because it seems rude to just walk out of a meeting with the reason: "I don't think I am adding or receiving value from this meeting". But I guess this is something that we need to get used to if we want to be more productive in our work - meeting really takes up too much of our time.

Side note: since I cannot leave the meeting, I zoned out during these meetings that I am not adding value, and focused on my other tasks. 8. Role of Middle Managers

Tesla’s CEO Elon Musk restructured the company’s management structure in 2018 to improve communication and increase efficiency. Facebook’s founder Mark Zuckerburg states that Facebook aspires its organisation structure to be flat, to be nimble, have more coaches than bosses, more facilitators than gatekeepers. The goal is to let people be in-charge of themselves and for communication to reach the key decision-makers as fast as possible so that decisions can be made fast. If we think about what middle management do, generally most of them break down tasks given to them from their bosses and pass them to be done by their subordinates. If their subordinates are managers, then the sub-task gets broken down into even smaller parts that are passed down to their subordinates – like the illustration I put below. Would it not be a lot more efficient if the first middle manager just split the tasks down into small components and pass it over to the associates, or if the associates themselves are formed in teams and each team is given a sub-task to complete (and how they would complete it is up to the team to split it among themselves).

But despite all the pros that might come with a flat organizational structure, the con is that there are limited positions available to promote amongst a huge pool of candidates, and some people no matter how good they are might just get stuck in a position forever because there are no seats at the top for them to promote to.

9. Agile / Scrum Leads to Faster Burnout

GIC is moving its development methodology to follow the Agile / Scrum framework. As part of our Scrum practice, we have daily standups with our supervisor to go through our progress from yesterday, our goals for today, and the problems that we faced. This part of Scrum felt stressful because what we do not want to do during the standup is to tell our supervisor that we did not manage to get anything done yesterday because we were trying to debug our program – it kind of made us look inefficient, which was something we did not want to portray. So what happened was we ended up working overtime quite a bit to try and get some tasks completed so that we have something to show the next day. This went on for almost two months and it felt extremely taxing and burnt me out that eventually I stopped and started saying “work in progress” when I faced a bug and could not resolve it by the end of the day. But apparently feeling burnt out is a common issue of Scrum, so it is not anyone's fault; it is just the way the framework is, and me being inexperienced about how Scrum works, worked tirelessly on tasks using the framework that led to my eventual burnout. So if you following the Agile framework, do a search online for ways to reduce your burnout.

Conclusion

I had a really great experience in GIC, and I learnt a lot.

If you are interested, APPLY!🤣

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF

Today's post: Basic Retirement Sum

It is one of the 3 types of Retirement Sum launched by CPF.

It is currently set at half the prevailing CPF Full Retirement Sum (FRS)

Why would someone wish to pledge their house in exchange for a "large" sum of money?

This post will answer that question.

For more information on the different types of Retirement Sums, click HERE

For more information on the amount on the different types of Retirement Sums, click HERE

Criteria for BRS

1) You need to have a house.

The house will be used and pledged against CPF.

Is your house fully paid or are you still paying it?*

2) You need to have money in excess of the BRS amount

The BRS amount from now until 2020 has been set.

For 2019, the BRS is set at $88,000 for those turning 55

For the years beyond, please look at our post HERE

Advantages

1) You get to withdraw your CPF money

No, you don't get to withdraw all your CPF money.

But you get to withdraw the amount that is in excess of your BRS.

So if your BRS is $90,000; you can withdraw from your CPF money in excess of that $90,000.

Disadvantages

1) Lower Monthly Payouts

Because you currently only have half the Full Retirement Sum (FRS), you will only get half of the monthly payout. But, you have withdrawn the excess amount.

2) You have to Return the Money to CPF

If you sold your house, you have to return the money you have taken out, back into the CPF.

BUT! You can still use the money in your CPF to buy another house and then apply for BRS again to get the excess money out if you have any. For more details, look at our post HERE

*If you have fully paid your house, you can pledge your house to withdraw money in excess of your BRS.

If you have not year fully paid your house, you can still withdraw the CPF money in excess of your BRS after pledging your house.

Your outstanding housing loan, however, will be paid with

a) your CPF OA money - if you are still working or if there is still money inside

b) with your cash - if your CPF OA has insufficient money to pay your monthly mortgage

The money in excess of BRS that you withdraw WILL NOT be forcefully used to immediately pay your housing loan.

For more concrete examples, you may refer to the link HERE and THERE Recommended Read: Why I am NOT Paying Back my Student Loan ASAP

Remember to offer your opinions. If you don't put your two cents in, how can you expect to get change?

Unhappy with your job? There's something you can do about it. A. Save up enough money from your job so that you can fire your boss - the problem is it might take some time and some effort B: Find a new job, search for new opportunities. A career coach might be able to help you with that. And if you are looking for a free career coach, visit Workforce Singapore via the link below. They can link you up with the career coach and you might be able to find new opportunities on their jobs portal. http://ow.ly/GY8150wlfrF